Bitcoin's Fading Diversification Benefit

Rising equity exposure, weaker downside protection, and shrinking portfolio benefits

Bitcoin has long been viewed as a portfolio diversifier, an asset that moves independently of stocks and cushions equity drawdowns. However, things have changed. Its correlation with equities has increased; its market beta has risen from essentially zero to roughly one; and the Sharpe ratio benefit of adding a 10% Bitcoin allocation to a portfolio has fallen sharply, although the magnitude depends on the underlying asset mix.

The Changing Correlation and Market Beta

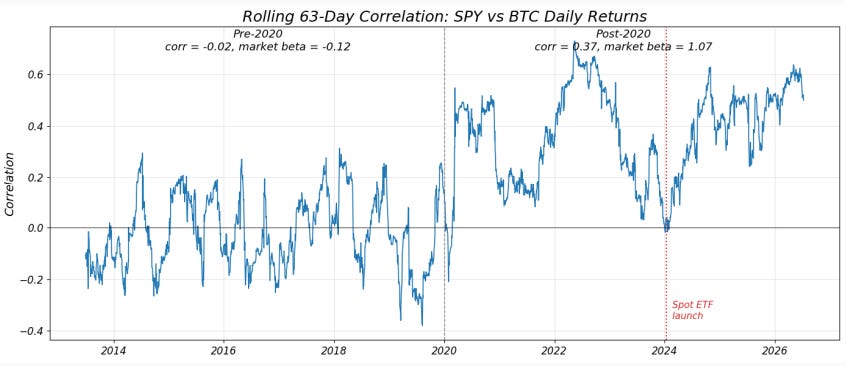

The rolling 3-month correlation between BTC and SPY daily returns tells the basic story. From 2013–2019, it oscillated between roughly -0.3 and +0.3 with no clear trend, an asset trading on its own idiosyncratic cycle, largely detached from equities. Since 2020, the whole distribution has shifted up, spending most of its time between 0.3 and 0.7.

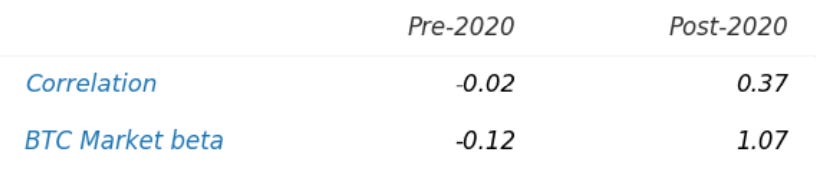

The full-sample correlation between Bitcoin and the S&P 500 is modest (0.16), but it obscures a pronounced regime change. Before 2020, the correlation was essentially zero (-0.02); since 2020, it has averaged 0.37. Investors relying on the full-sample estimate would therefore materially understate Bitcoin's current relationship with equities.

The shift is even clearer when looking at market beta. Before 2020, Bitcoin's market beta was -0.12, implying essentially no systematic equity exposure. Since 2020, it has increased to 1.07, meaning a dollar invested in Bitcoin now carries roughly the same market risk as a dollar invested in the S&P 500. That's not a subtle change. Bitcoin went from behaving largely as an unrelated asset to behaving much more like an equity position.

What might explain this shift? The timing is consistent with a growing literature on Bitcoin’s financialization. An IMF working paper (Che et al., 2023) identifies a common “crypto factor” whose correlation with global equities rose sharply after 2020 as institutional participation increased and the marginal crypto and equity investor became increasingly similar. Conlon and McGee (2020) showed that Bitcoin failed to act as a safe haven during the March 2020 market crash, while Nguyen (2022) found that S&P 500 returns began exerting a stronger influence on Bitcoin returns during periods of high uncertainty.

The rolling correlation also exhibits a second upward shift in early 2024, coinciding with the launch of US spot Bitcoin ETFs on January 11. Around that event, the 30-day rolling correlation increased from roughly 0.02 immediately before the launch to around 0.28 immediately afterwards. While this evidence is descriptive rather than causal, it is consistent with the hypothesis that spot ETFs further integrated Bitcoin into mainstream investment portfolios, as discussed in Hong et al. (2025).