Building a Smarter TAA Model for Stronger Returns and Lower Risk

Incremental Enhancements to a Tactical Asset Allocation Strategy: Boosting Sharpe Ratios and Reducing Downside Risk

Hello,

A quick note before we dive in: Starting now, my Research Insights posts will be published on Sundays. This new schedule not only brings you fresh ideas and research right before the trading week begins, but also aligns better with my workflow, allowing me to dedicate more time to producing high-quality, actionable content for you.

This week, I’m revisiting the tactical asset allocation framework I’ve shared with you before. Over the past several posts, we’ve explored a series of enhancements, each aimed at making the original model more robust, risk-aware, and effective. Now it’s time to bring all those improvements together and see how the fully upgraded version performs when tested as a complete system.

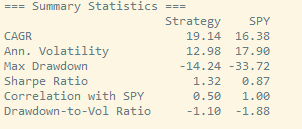

Overall, the results are quite attractive. Across different choices of equity exposure, the enhanced TAA model delivers CAGRs between 12% and 27% after costs, Sharpe ratios around 1.3, and modest drawdowns, maintaining strong downside protection. Below are examples of how the model performs when rotating into different equity exposures:

Rotating into SPY

Rotating into SSO

Rotating into SPXL

More on the model below.