Recessions and Market Timing

Is the Sahm rule useful for market timing?

Hi there, it’s time for another article. This one explores the impact of recessions on stock returns, recent research on recession indicators, and whether there are any benefits to market timing with these indicators. Make sure to subscribe to receive future posts.

Introduction

The release of unemployment figures on August 2 has ignited a debate on whether the U.S. economy has entered a recession. The Sahm Rule, a well-known recession indicator, suggests that a recession might have begun, while recent academic research indicates that a recession may have started months ago. This blog post explores the relationship between past recessions and stock market returns, reviews the academic literature on recession indicators and the predictability of economic growth, and conducts a market timing exercise using the Sahm rule. I conclude with key takeaways for investors.

Table of Contents

· Recessions and Stock Returns

· Recession Indicators: A Literature Review

· Market Timing

· References

Recessions and Stock Returns

To understand the impact of past recessions on stock market returns, I plot recession periods identified by the National Bureau of Economic Research (NBER), obtained from the FRED database, against cumulative market excess returns for the broad U.S. stock market, sourced from Kenneth French’s data library. The NBER defines a recession as "a significant decline in economic activity that is spread across the economy and lasts more than a few months," and is determined retrospectively. The figure below shows that certain recession periods have led to significant equity drawdowns, notably during the 1930s, 1970s to 1980s, and 2000s. The U.S. has been in a recession 17% of the time based on the number of recession months relative to the entire sample period.

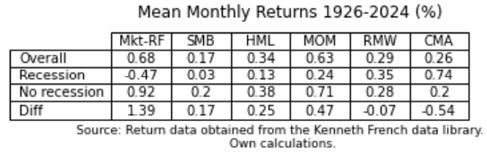

The table below summarizes average monthly market returns during all periods, as well as specifically during recession and non-recession periods. It also includes average returns for the size (SMB), value (HML), momentum (MOM), profitability (RMW), and investment (CMA) factors, sourced from Kenneth French's data library.

Historically, market returns have been significantly lower during recession periods, whereas momentum and the Fama-French factors show less pronounced differences. Notably, the investment factor has performed well during recessions over the course of the nearly 100-year sample period.

Starting from 1985, the substantial disparity between market portfolio returns in recession and non-recession periods persists, as illustrated below. The table also indicates that the value and momentum factors have underperformed during recessions, while the profitability factor has exhibited the opposite trend. Note that only about 8% of the months since 1985 have been recession months.

Recession Indicators: A Literature Review

The NBER dates recessions retrospectively, meaning these periods are not known to investors in real-time. However, past research has introduced several real-time recession indicators. The Sahm Rule, proposed by Sahm (2019), signals a recession when the three-month moving average of the U.S. unemployment rate rises by 0.5 percentage points or more above its lowest three-month average over the previous 12 months. The figure below illustrates the real-time application of the Sahm Rule, sourced from the FRED database, alongside the NBER-defined recession periods. The most recent data point surpasses the 0.5 threshold.

In a recent paper, Philips (2024) evaluates the effectiveness of the Sahm indicator in identifying recessions and concludes that, while it performs reasonably well, it often signals a recession 3 to 6 months late. This delay is not unexpected, as the unemployment rate is generally considered a lagging indicator. To improve timeliness, Philips proposes a new recession indicator combining the unemployment rate with the yield curve slope. This new indicator is found to be timelier and suggests that the U.S. economy may have already entered a recession as early as July 2024.

The yield curve slope as an indicator of economic activity has been extensively researched. Early studies by Harvey (1989), Estrella and Hardouvelis (1991), and Estrella and Mishkin (1996) demonstrate that the spread between long-term and short-term interest rates positively predicts economic growth out-of-sample. Specifically, a flattening or inversion of the yield curve is often seen as a signal of an impending recession. This is evident in the figure below, which also shows that the timing between yield curve inversions and subsequent recessions can vary.

Rudebusch and Williams (2009) document that the yield curve slope serves as a more effective real-time predictor of recessions compared to professional forecasters. Engstrom and Sharpe (2019) find that a short-term forward spread on Treasury bills is a superior predictor of recessions than spreads involving longer-term interest rates, as it more accurately reflects investors’ expectations regarding monetary policy. Recently, Abbritti et al. (2024) find that incorporating changes in the yield curve slope, in addition to the slope itself, improves the prediction of recessions and economic activity.